Warehouses are stockpiling a real estate value play

The European logistics market has so far missed out on the green revolution underway in the real estate sector. But with clear cost benefits emerging for sustainable assets and a valuation repricing on the way, now is the time to reduce the carbon footprint of one of real estate’s biggest segments.

Originally published in April 2023 by Fidelity International.

Written by Maarten Frouws, Investment Manager, Real Estate, Cian O-Sullivan, Analyst, and Nina Flitman, Senior Writer.

The Netherlands is the logistics heart of Europe. The small country has the largest seaport in the region, a major airport hub, and around 41 million square metres of warehouses and distribution centres, equal to about 6,000 football pitches.

Visit an average Dutch warehouse, covering around 25,000 square metres, and you will be greeted by what is already a fairly energy-efficient property. Energy use intensity (EUI) for these types of buildings is an estimated 86 kWh per metre square1 compared with 250 kWh/m2 for offices or 150–175 kWh/m2 for homes2. But despite this head start, there are still significant improvements that can – and should, if Fidelity International is to reach its net zero goals – be made. And while most of Europe’s domestic and office real estate is getting to grip with its carbon footprints, the logistics segment, one of the largest components of the asset class, has so far been left behind.

Taking stock of sustainability

In Europe, logistics assets account for 421 million square metres3, almost the same area as Barbados, with nearly 32 million sqm of new space snapped up across 13 countries in 20224. In England alone, storage and warehousing properties take up 126 million sqm – more than offices (74 million sqm), retail (115 million sqm), or landfill (20 million sqm)5. But sustainability has not been a priority for this enormous sub-sector. As of late 2022, the average share of BREEAM-certified stock in industrials and logistics investment volumes was only 8.1%6.

While warehouses and distribution centres typically use less energy relative to their size than offices or homes (they’re less likely to be heated, for example), there is still a growing demand for green assets in the logistics space. And although there is little research on how much occupiers or investors are willing to pay for these green buildings, emerging data sets are beginning to make a strong economic case for improving their sustainability.

For example, even with less heating, energy costs are still weighing on occupiers. The tenants of the Dutch warehouse in one example Fidelity International has looked at can expect to face annual energy costs of around 775,000 euros7, or around 26.7% of total occupancy costs8. However, Fidelity International’s analysis suggests that upgrades could see the EUI of a building like this cut to around 28 kWh/m2, suggesting a total annual energy cost of just 250,000 euros, a two-thirds reduction. In these cases the proportion of occupancy cost spent on energy would come down to around 10.6% (presuming that no green premium was applied and annual rent remained around 2.1 million euros).

Occupiers are beginning to take note of figures like these. A survey of the logistics real estate market in 2022 from estate agency Savills showed that green features are considered “very important” or “important” by 65% investors, with the remaining 35% saying they are “slightly” or “moderately” important9.

And it seems that buyers are willing to pay up to meet their appetite for sustainable assets. Research from CBRE, a commercial real estate firm, suggests that U.K. logistics assets with a BREEAM rating of excellent have a 30-basis-points median valuation premium compared to market prime net yield.

New regulation is also likely to increase demand for sustainable logistics space. In the U.K., the Minimum Energy Efficiency Standards that require commercial rents to net certain energy performance certificates (EPC) ratings will begin to apply to logistics assets over the next few years, while similar rules are emerging across various European jurisdictions. Buildings that are not updated risk becoming stranded assets that cannot be rented and only sell at a discount.

Pressure growing

The carbon footprint of logistics is moving up agendas as activity in the industry and demand for space grows, fuelled by a retail sector that continues to shift online and relies more heavily on warehouses and distribution centres. In the U.K., for example, it’s estimated that for every one billion pounds’ growth in online retail, some 72,000 m2 of new warehouse space is needed10 – or about 10 football pitches. Some 89% of occupiers anticipate they will need the same or more space in the next three years11, while supply chain realignment through reshoring and higher inventory retention means that both manufacturers and third-party logistics providers predict a need for more space.

Not only does Fidelity International expect to see new logistics infrastructure built with sustainability front of mind but more and more existing warehouses and distribution centres will be retrofitted, either with simple upgrades such as more efficient LED lighting, or more complex transformations involving heat pump installations or using warehouses’ flat rooves for solar panels.

High demand combined with low vacancy rates is already fuelling rental growth across much of Europe’s logistics market. An index from commercial real estate company JLL showed rents rising 14.2% year-on-year during the third quarter of last year12.

Repricing on the way

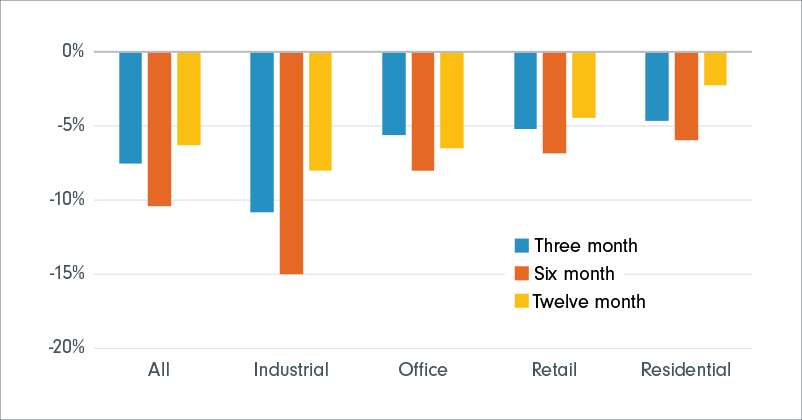

Although rental premiums remain high, prices in the industrials real estate sector have been far below where they were just a year ago. However, this suggests there is now a discount window available before the cycle turns and a potential repricing comes into effect. According to data from MSCI, industrials – which includes logistics assets such as warehouses and distribution centres – is valued 8% below where it was this time in 2022, by far the greatest discount offered by any sector. The U.K. is seeing the largest year-on-year fall in industrials valuations at 16.9%, with London at 18.5%.

Back at the Dutch warehouse, these latest figures would imply a fall in its value of 10.4% over the last year, or 11.2% if it were in Rotterdam. A repricing along with any green renovations would be a big boost for its valuation, with benefits delivered to the owner, the tenant and to the net-zero transition.

1Towards cost-effective nearly zero energy buildings: The Dutch Situation, Wim Zeiler, Kristian Gvozdenović, Kevin de Bont, and Wim Maassen; Science and Technology for the Built Environment, July 2016.

2The Value of Actual Energy Performance in the Dutch Private Residential Sector: A Quantitative Approach, Niels Fine.

3ERIX Market Data as of Q4 2022, CBRE.

4European Logistics Market Update, JLL, February 2023.

5Land use in England, 2022, Department for Levelling Up, Housing and Communities, October 2022.

6Capturing the value of sustainability in European logistics, CBRE Research, September 2022.

7For an asset with an Energy Use Intensity of 86 kWh per square metre.

8Based on rent of just over 2.1 million euros.

92022 European Real Estate Logistics Census, Savills, Autumn 2022.

10The size and make up of the UK warehousing sector, 2021, UKWA.

112022 European Real Estate Logistics Census, Savills, Autumn 2022.

12European Logistics Market Update, JLL, November 2022.

Issued by Fidelity Investments Canada ULC (“FIC”). Unless otherwise stated, all views expressed are those of Fidelity International, which acts as a subadvisor in respect of certain FIC institutional investment products or mandates.

For institutional use only.

This document is for investment professionals only and should not be relied on by private investors.

This document is provided for information purposes only and is intended only for the person or entity to which it is sent. It must not be reproduced or circulated to any other party without the prior permission of Fidelity.

This document does not constitute a distribution, an offer or solicitation to engage the investment management services of Fidelity, or an offer to buy or sell or the solicitation of any offer to buy or sell any securities in any jurisdiction or country where such distribution or offer is not authorized or would be contrary to local laws or regulations. Fidelity makes no representations that the contents are appropriate for use in all locations or that the transactions or services discussed are available or appropriate for sale or use in all jurisdictions or countries or by all investors or counterparties.

This communication is not directed at and must not be acted on by persons inside the U.S. and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorized for distribution or where no such authorization is required. Fidelity is not authorized to manage or distribute investment funds or products in, or to provide investment management or advisory services to persons resident in, mainland China. All persons and entities accessing the information do so on their own initiative and are responsible for compliance with applicable local laws and regulations and should consult their professional advisors.

Reference in this document to specific securities should not be interpreted as a recommendation to buy or sell these securities but is included for the purposes of illustration only. Investors should also note that the views expressed may no longer be current and may have already been acted upon by Fidelity. The research and analysis used in this documentation is gathered by Fidelity for its use as an investment manager and may have already been acted upon for its own purposes. This material was created by Fidelity International.

This article has been provided by Fidelity Investments Canada ULC (Fidelity) and is for information purposes only. It comprises, among other things, examples of sustainable investing activities across Fidelity and FIL Limited (Fidelity International) only, current as of March 31, 2023. The article may refer to ESG considerations that Fidelity and Fidelity International may take into account as part of their research or investment process, and is not necessarily reflective of the approach of any other Fidelity Investments company or sub-advisor, such as Fidelity Management & Research Company LLC, FIAM LLC, Geode Capital Management, LLC, and State Street Global Advisors Ltd., to ESG research, stewardship and sustainable investing, either specifically or generally.

Past performance is not a reliable indicator of future results.

This document may contain materials from third parties which are supplied by companies that are not affiliated with any Fidelity entity (third-party content). Fidelity has not been involved in the preparation, adoption or editing of such third-party materials and does not explicitly or implicitly endorse or approve such content.

Fidelity International refers to the group of companies which form the global investment management organization that provides products and services in designated jurisdictions outside of North America. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. Fidelity only offers information on products and services and does not provide investment advice based on individual circumstances.

©2023 Fidelity Investments Canada ULC. All rights reserved.