Thoughts on the software reset for private credit

Fidelity’s direct lending team explores current conditions for software equities following a sharp decline, and where they are finding opportunities in more resilient segments of the market.

Originally published in February 2026 by our U.S. partners.

Written by David Gaito, CFA, Head of Direct Lending.

Highlights

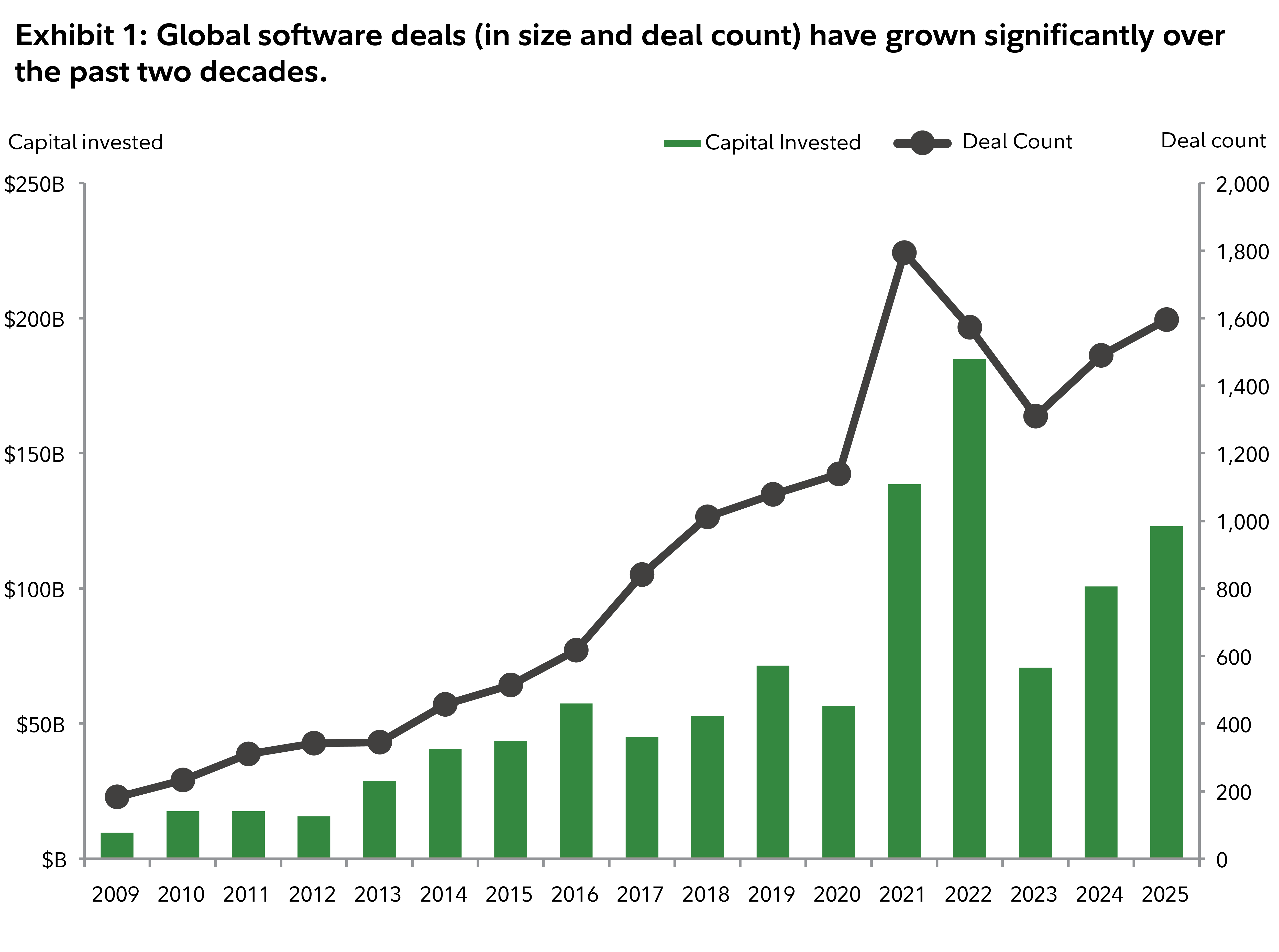

- Software equities have experienced a sharp drawdown, but the current reset may ultimately create a healthier lending environment than what has prevailed in periods where assets were overvalued and financed with aggressive leverage.

- Software has represented less than 10% of our direct lending investment activity over the past several years, reflecting our belief that there was indiscriminate excess focused more on loanto-

values (LTV) than business fundamentals. - Such periods of pronounced volatility in public software markets tend to reshape capital availability, risk appetite, and, ultimately, transaction terms across the private markets. Several areas of mission-critical software should be resilient, such as cybersecurity and compliance infrastructure, enterprise controls, and secure data environments (including health care).

Source: Pitchbook Data Inc., as of 12/31/25.